Diversification in a Dollar-Bear World: What Non-Correlated Strategies Offer Now

For much of the past decade, U.S. investors benefited from an unusually strong dollar. That tailwind is beginning to fade. By multiple valuation measures, the dollar appears stretched, while rising fiscal deficits, persistent trade imbalances, and shifting global reserve practices are increasing pressure on the currency.¹ Analysts increasingly argue that conditions are forming for a prolonged period of dollar weakness.² If that view proves correct, portfolios built primarily around dollar-denominated assets may face a different risk profile than investors have grown accustomed to.

A weakening dollar tends to alter market relationships. Import prices rise, commodity prices often firm, and overseas earnings translate more favorably for U.S. multinationals.² At the same time, non-U.S. equities have historically outperformed during sustained dollar declines, reflecting both currency translation effects and improving relative growth dynamics abroad.³ These shifts highlight the importance of diversification strategies that are not tightly linked to the dollar itself.

Broadening Currency Exposure

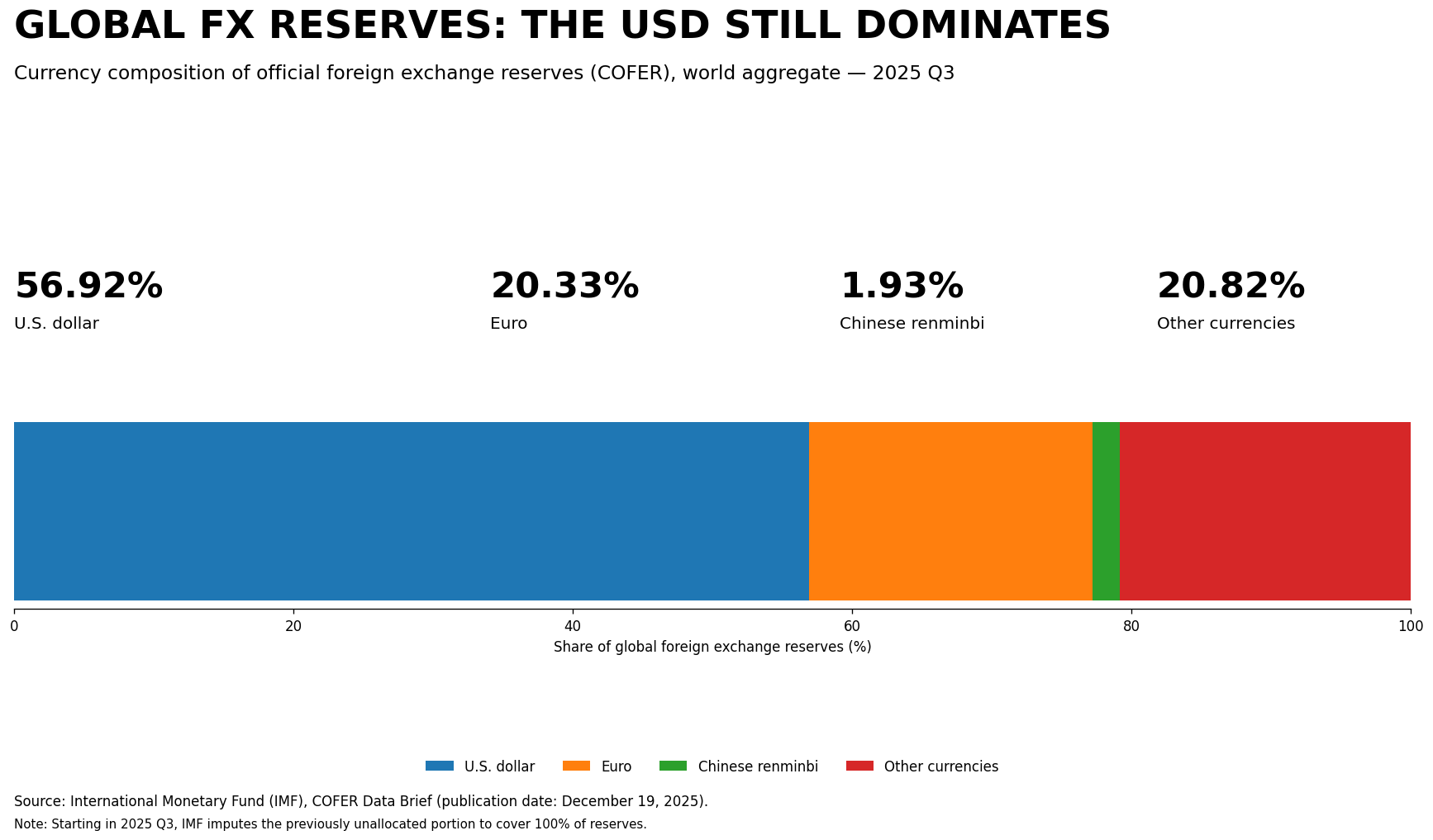

One response to a softer dollar environment is broader currency diversification. Although the U.S. dollar remains the world’s primary reserve currency, its share of global foreign exchange reserves has declined meaningfully over the past decade.¹ Central banks have increasingly diversified into other currencies, and into gold in particular, signaling a gradual move toward a more multipolar monetary system.¹

For investors, foreign assets offer implicit currency exposure. Unhedged international equities and bonds allow portfolio returns to benefit if foreign currencies appreciate relative to the dollar.⁴ Major currencies such as the euro and yen have historically strengthened during dollar downcycles, providing an additional layer of diversification beyond equity returns alone.³ While currency exposure can introduce volatility, the objective is not to predict exchange rates but to reduce over-reliance on a single currency regime.

Commodities and Real Assets

Commodities have long been viewed as beneficiaries of dollar weakness. Because most commodities are priced in dollars, a declining dollar tends to support higher nominal prices by boosting global demand.⁵ Energy, industrial metals, and agricultural commodities have all demonstrated this relationship during prior dollar bear markets.⁵

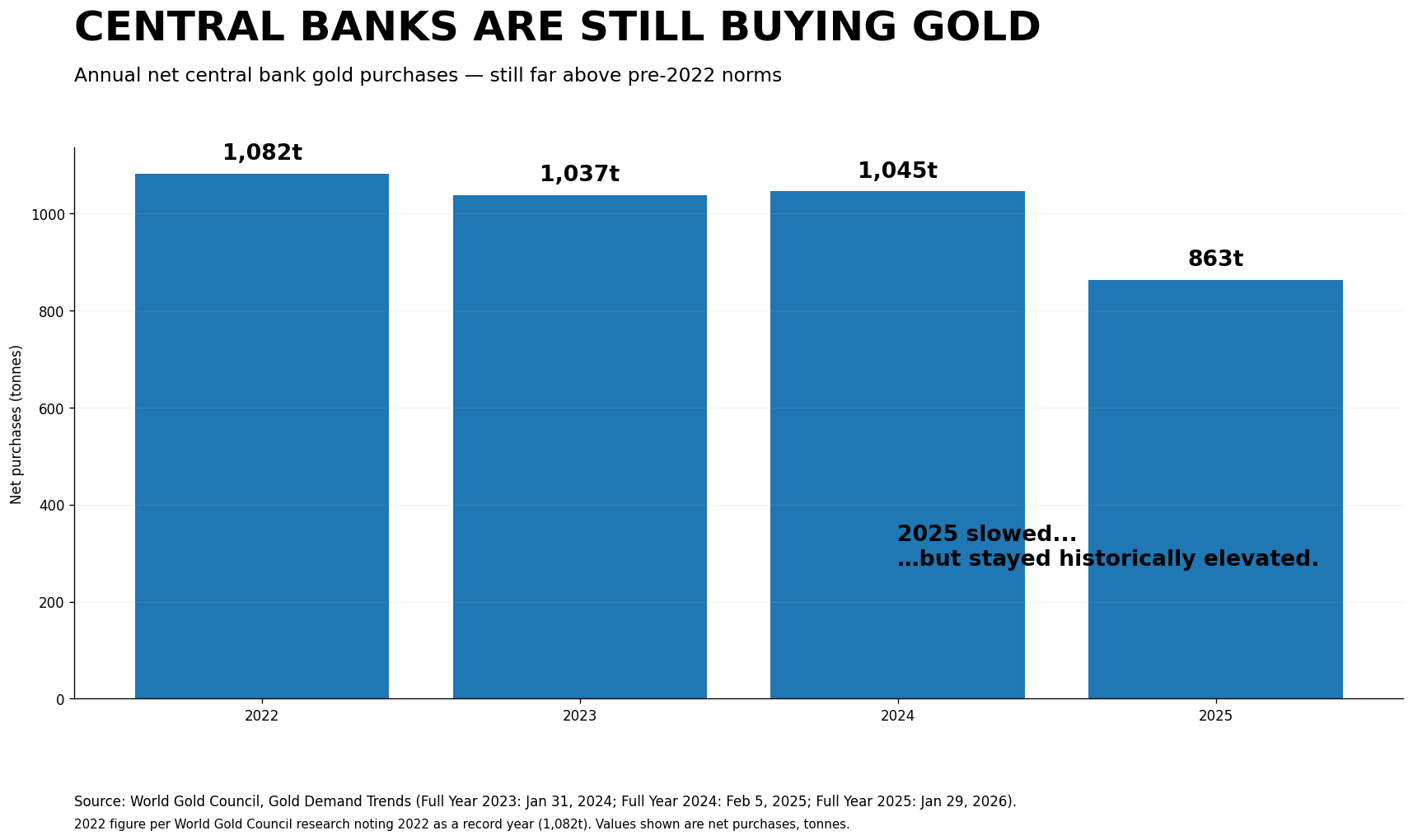

Gold occupies a distinct role within this group. Its historical inverse correlation with the dollar has made it a widely used store of value during periods of currency stress.⁶ Recent years have reinforced that reputation, with gold prices reaching record levels amid concerns about inflation persistence, fiscal sustainability, and long-term currency credibility.⁶ Central bank accumulation of gold further underscores its function as a reserve asset outside the fiat currency system.¹

Managed Futures as a Structural Diversifier

Beyond asset-based diversification, strategy-based approaches can also play a role. Managed futures strategies seek to capture sustained trends across equities, bonds, commodities, and currencies using futures contracts. Over long periods, these strategies have exhibited low correlation to both stocks and bonds, particularly during market stress.⁷

Their flexibility allows them to adapt to macro shifts, including prolonged dollar weakness, by dynamically adjusting exposures rather than relying on static allocations. While managed futures are not immune to drawdowns and require patience, their historical tendency to perform well during periods of broad market dislocation has made them a notable complement to traditional portfolios.⁷

Bottom line: A dollar-bear environment challenges assumptions formed during years of dollar strength. Incorporating assets and strategies with lower dollar dependence can improve portfolio resilience. No single approach offers certainty, but thoughtful diversification across currencies, real assets, and alternative strategies can help investors navigate a changing monetary landscape with greater balance and flexibility.

Footnotes

Morgan Stanley Investment Management. The Big Picture: Key Themes for 2023. February 1, 2023.

J.P. Morgan Private Bank. Is This the Downfall of the U.S. Dollar? April 24, 2025.

Steve Brice et al. Global Market Outlook: Positioning for a Weak Dollar. Standard Chartered, June 20, 2025.

BlackRock Investment Institute. 2025 Fall Investment Directions: Rethinking Diversification. August 25, 2025.

David Brower. What Assets Have Traditionally Done Best in a Weaker Dollar? Thrive Wealth Advisors, November 5, 2025.

J.P. Morgan Private Bank. Is It a Golden Era for Gold? January 2026.

Andrew Beer. Why Managed Futures Funds Are Ripe for Replication. Institutional Investor, September 5, 2023.

This material presented by Dynamic Wealth Group (“DWG”) is for informational purposes only and is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy, or investment product. Facts presented have been obtained from sources believed to be reliable, however DWG cannot guarantee the accuracy or completeness of such information, and certain information presented here may have been condensed or summarized from its original source. DWG does not provide legal or tax advice, and nothing contained in these materials should be taken as legal or tax advice.