Scarcity Pricing vs Visible Stocks: Why Copper Inventories Can Rise While the Bull Case Survives

The Moment That Confused the Market

Anyone who’s bought wiring, plumbing, or even a new appliance has felt copper’s fingerprints on the receipt. Copper has stayed pricey, which makes the latest headline feel backward: exchange inventories have jumped at the same time prices stayed elevated.¹

The catalyst is simple and strange. Global exchange stocks have risen sharply since the start of January, with big builds showing up in U.S. warehouses tied to COMEX and in China’s exchange system.¹ Even the London warehouse network has seen a steady run of inflows, pushing reported stocks higher over consecutive sessions.² When you hear that inventories are rising, the reflex is to think demand must be rolling over.

That reaction isn’t irrational. High prices can slow orders, delay projects, and encourage substitution. Reuters noted that this rally has started to curb near-term manufacturing appetite, even as metal keeps flowing into visible storage.¹ The twist is that visible storage is not the same thing as available supply, and copper’s price often reflects scarcity in the wrong place at the wrong time, not abundance somewhere else.

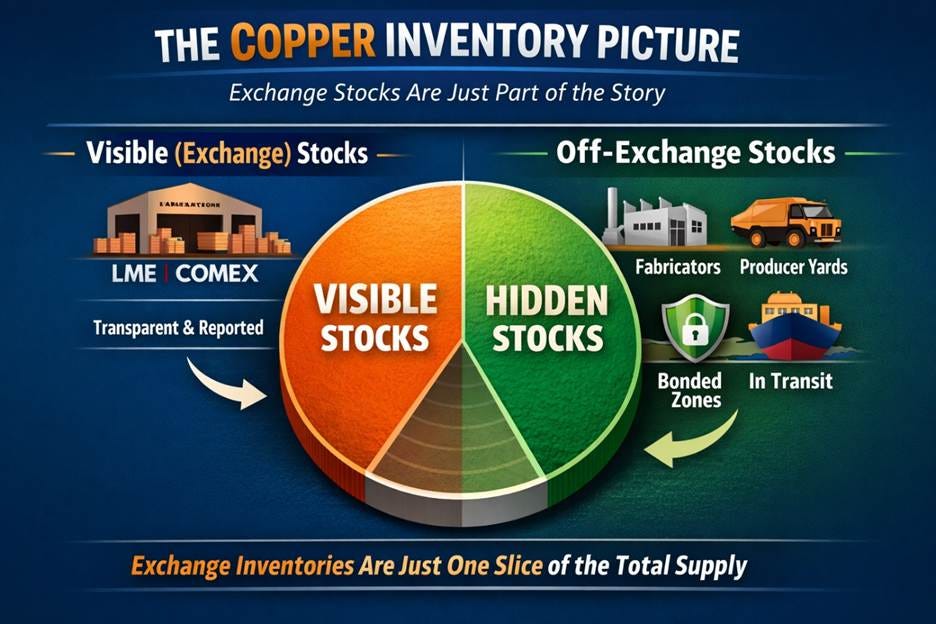

What “Visible Stocks” Really Measure

Exchange inventories are a very specific slice of the copper universe: metal that sits in exchange-linked warehouses, measured and reported under exchange rules. That dataset matters because it anchors deliverability for futures contracts and shapes the short-term plumbing of price discovery.²

The dataset also has blind spots. A large share of copper lives off-exchange: at fabricators, in producer yards, inside bonded zones, on ships, or sitting as semi-finished product. The metal can be real and usable without showing up in the daily stocks screenshot that traders pass around.

Exchanges have tried to close part of that gap. The London Metal Exchange expanded transparency on off-warrant metal held inside its warehouse network because market participants wanted a more complete picture than on-warrant stocks alone.³

Another wrinkle is that the same ton can move without, well, actually moving. Metal can shift from off-warrant to on-warrant. It can also relocate across regions because spreads, tariffs, and financing incentives change.

Reuters described exactly that kind of distortion: tariff uncertainty and price gaps pulled material into the United States, swelling U.S.-linked inventories while altering availability elsewhere.¹

Why the Bull Case Can Survive a Stock Build

Inventory builds can coexist with a structurally bullish story when the build is driven by relocation, timing, and risk management rather than by a true, lasting surplus.

Start with the curve. When copper is genuinely scarce, the front end of the market often shows stress. When it isn’t, the market relaxes.

In mid-February, the cash-to-three-month spread sat at a discount, signaling limited urgency for immediate delivery even as spot prices rebounded.² That’s a message about near-term tightness, not a verdict on the next decade.

Now zoom out.

The long-cycle argument for copper never depended on inventories staying low every week. It depends on demand growth colliding with slow supply response. The International Energy Agency expects copper demand to rise materially over time, driven by grid expansion and electrification, and it also warns that the announced project pipeline falls short of projected needs in the 2030s under today’s policy settings.⁴

That gap matters because copper projects take years to permit, build, and ramp, and ore quality trends have pushed costs higher.⁴

The concentrate market tells a similar story. Smelter treatment and refining charges have remained under heavy pressure, which industry participants often read as a sign that mine supply of clean concentrate has stayed tight.⁵ Rising exchange inventories may soften the tape for a while, yet a tight upstream pipeline can keep the bigger thesis intact.

Investors should treat this episode as a reminder to separate the tactical from the structural. Visible stocks can rise because traders park metal where the rules and incentives are favorable. Scarcity pricing can persist when the market still worries about medium-term supply, project delays, and the capital required to keep up.

The risk is straightforward: if inventories keep rising and the curve stays relaxed, the market may be telling you the cycle is cooling faster than the narrative. The opportunity is equally clear: structural demand does not arrive all at once, and copper often offers better entry points when the mood turns from certainty to confusion.

Footnotes

Reuters, Andy Home, “Copper is pricing scarcity at a time of plenty,” February 13, 2026.

Tom Daly, “Copper climbs on dip-buying, tech shares recovery,” February 18, 2026.

London Metal Exchange, “LME provides daily insight into off-warrant stocks,” March 17, 2025.

International Energy Agency, “Overview of outlook for key minerals,” Global Critical Minerals Outlook 2025, May 21, 2025.

S&P Global, Lu Han, “TRADE REVIEW: Tight copper concs supply to keep smelter margins under pressure in Q1,” January 12, 2026.

This material presented by Dynamic Wealth Group (“DWG”) is for informational purposes only and is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy, or investment product. Facts presented have been obtained from sources believed to be reliable, however DWG cannot guarantee the accuracy or completeness of such information, and certain information presented here may have been condensed or summarized from its original source. DWG does not provide legal or tax advice, and nothing contained in these materials should be taken as legal or tax advice.