Tariff Tensions Escalate: The Macro Market Impact of Renewed U.S.–Europe Trade Threats

Talk of tariffs has returned to the center of market discourse, and the catalyst has been as unexpected as it is unsettling. A renewed dispute between the United States and several European allies, tied to Greenland, has revived fears of a broader transatlantic trade conflict. What initially appeared to be geopolitical theater quickly translated into market stress, reminding investors how sensitive global assets remain to policy-driven uncertainty.

Equities Reprice Political Risk

Equity markets reacted swiftly as investors attempted to assess the economic consequences of revived tariff threats. European stocks bore the brunt of the initial selloff, particularly sectors with deep exposure to U.S. demand. Automakers, industrial exporters, and luxury goods producers led declines as traders reassessed earnings assumptions under a potential tariff regime. The selloff reflected less a precise forecast of policy outcomes than a broader repricing of uncertainty. Trade disputes disrupt supply chains, compress margins, and delay corporate investment decisions, all of which undermine confidence in forward earnings.

A handful of defense and aerospace names moved higher, reflecting speculation that Europe may respond to heightened geopolitical pressure by increasing strategic spending. Those gains, however, were isolated. Overall, equities signaled a clear shift toward risk aversion. Futures markets suggested U.S. stocks would follow once trading resumed, reinforcing the notion that tariff rhetoric alone can be sufficient to reverse sentiment even before concrete measures are enacted.

Commodities Signal a Flight to Safety

Commodity markets delivered a more decisive verdict. Precious metals surged as investors sought insulation from political and monetary uncertainty. Gold and silver prices pushed to record levels, reflecting a renewed preference for assets perceived as independent of government policy and financial systems. Historically, tariff episodes tend to bolster safe-haven demand, particularly when they coincide with concerns about inflation and currency stability.

Energy markets told a more nuanced story. Oil prices, which had recently been supported by supply-related geopolitical risks elsewhere, flattened as trade tensions raised doubts about future global demand. The prospect of slower growth offset earlier supply fears, leaving crude prices rangebound. Industrial metals also remained firm, partly because the dispute highlighted the strategic importance of resource security. Greenland’s mineral wealth underscored a broader trend toward resource nationalism, reinforcing investor interest in tangible inputs to the real economy.

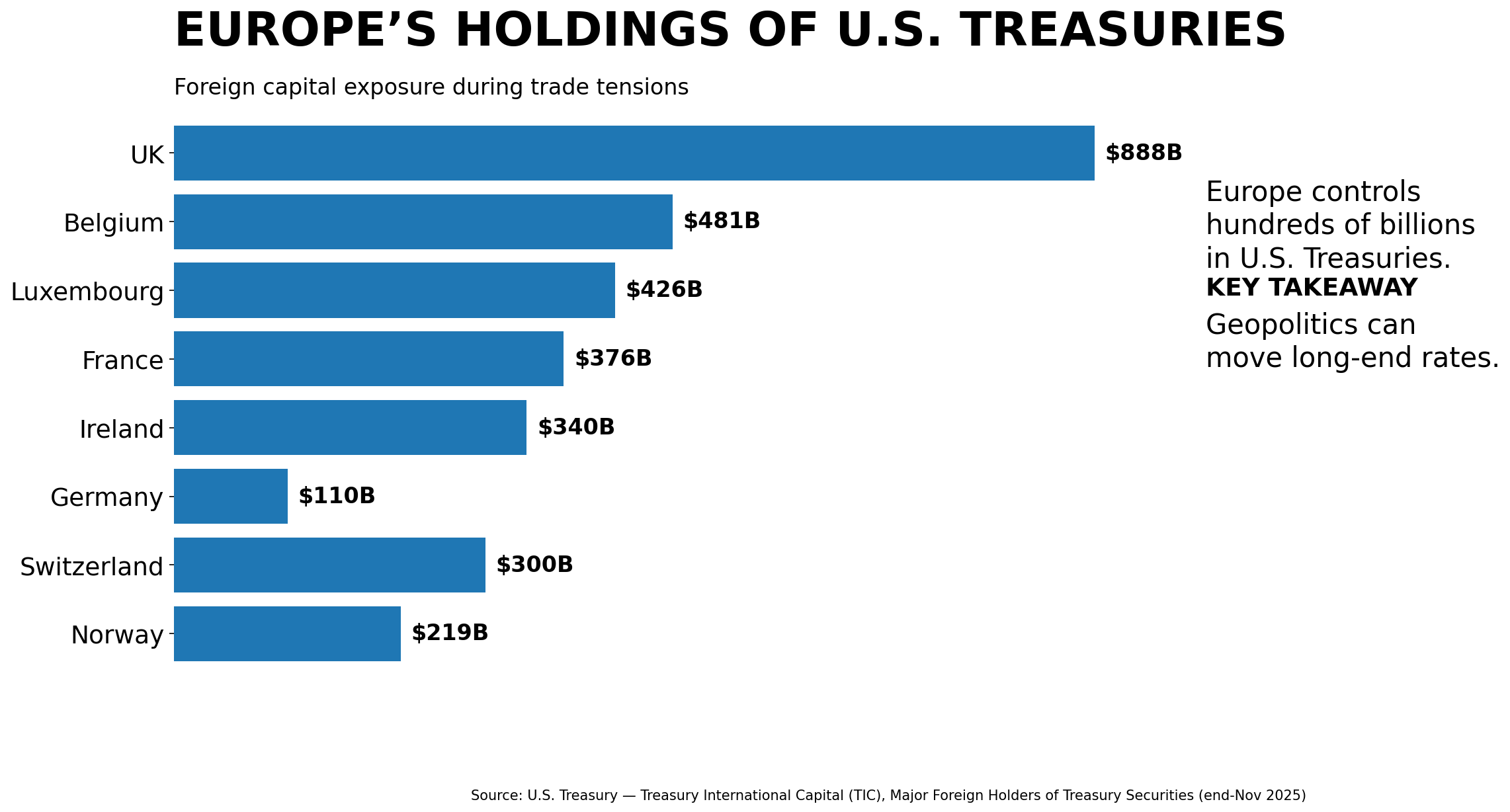

Bonds, Real Yields, and Policy Expectations

The bond market response was less conventional. European government bonds attracted inflows as local investors sought safety, pushing yields lower. In contrast, longer-dated U.S. Treasury yields moved higher, suggesting unease about America’s reliance on foreign capital at a time of escalating political friction. Speculation that Europe could respond to tariff pressure through financial channels introduced a new layer of risk for U.S. debt markets.

These moves fed directly into real yields. Tariffs are inherently inflationary, as they raise import costs, yet they also threaten growth. Markets began to price a scenario in which inflation expectations drift higher while central banks remain inclined toward accommodation to cushion economic damage. The result is downward pressure on real yields, a dynamic that historically favors gold and other non-yielding assets.

For investors, the bond market’s message is cautionary. It reflects expectations of policy strain rather than confidence in a smooth resolution. Central banks may soon be forced to balance price pressures against slowing activity, a challenge that rarely produces stable markets.

Conclusion

A dispute over Greenland has reignited a familiar macro risk: trade conflict. The market reaction has followed a recognizable pattern, with equities retreating, safe havens rallying, and bond markets signaling unease. Whether this episode fades into negotiation or escalates into sustained confrontation remains uncertain. What is clear is that geopolitical risk remains a powerful driver of cross-asset performance. For portfolio construction, diversification and awareness of policy risk remain essential as markets navigate another reminder of how quickly political developments can reshape the macro landscape.

Footnotes

Michael Martina and Jason Lange, “Trump Vows Tariffs on Eight European Nations Over Greenland,” Reuters, January 17, 2026.

Adam Jourdan, Christoph Steitz, and Sybille de La Hamaide, “Trump’s Greenland Threat Puts Europe Inc Back in Tariff Crosshairs,” Reuters, January 19, 2026.

Kalyeena Makortoff and Lauren Almeida, “European Stock Markets Fall as Trump Renews Tariff Threats,” The Guardian, January 19, 2026.

Ayushman Ojha, “Gold Hits Record High on Tariff Fears,” Investing.com, January 19, 2026.

Amanda Stephenson, “Oil Steadies as Trade Tensions Offset Supply Risks,” Reuters, January 19, 2026.

Jason Ma, “Europe’s Potential ‘Sell America’ Response to Trade Tensions,” Fortune, January 18, 2026.

This material presented by Dynamic Wealth Group (“DWG”) is for informational purposes only and is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy, or investment product. Facts presented have been obtained from sources believed to be reliable, however DWG cannot guarantee the accuracy or completeness of such information, and certain information presented here may have been condensed or summarized from its original source. DWG does not provide legal or tax advice, and nothing contained in these materials should be taken as legal or tax advice.