U.S. Dollar Short, British Pound Long: Capital Flows Tell the Story

Global capital has begun to tilt toward the United Kingdom, weakening the U.S. dollar while lending support to the British pound¹. Investors appear to be reducing exposure to U.S. assets and redeploying capital across the Atlantic. The shift shows up clearly in currency markets: sterling has firmed against a softening dollar even as inflation remains above target in both economies².

The root cause lies in relative asset demand. As one strategist observes, “currency values reflect the global flow of funds”³. When investors move capital abroad, the dollar tends to sag. That dynamic intensified in early 2025, when U.S. tariffs reignited inflation fears and traders began pricing in deeper Federal Reserve rate cuts⁴. Policy uncertainty, coupled with slower growth expectations, has weighed on the greenback. Some bond managers now describe the dollar as “overvalued” versus the pound⁵—a signal that sentiment has shifted decisively.

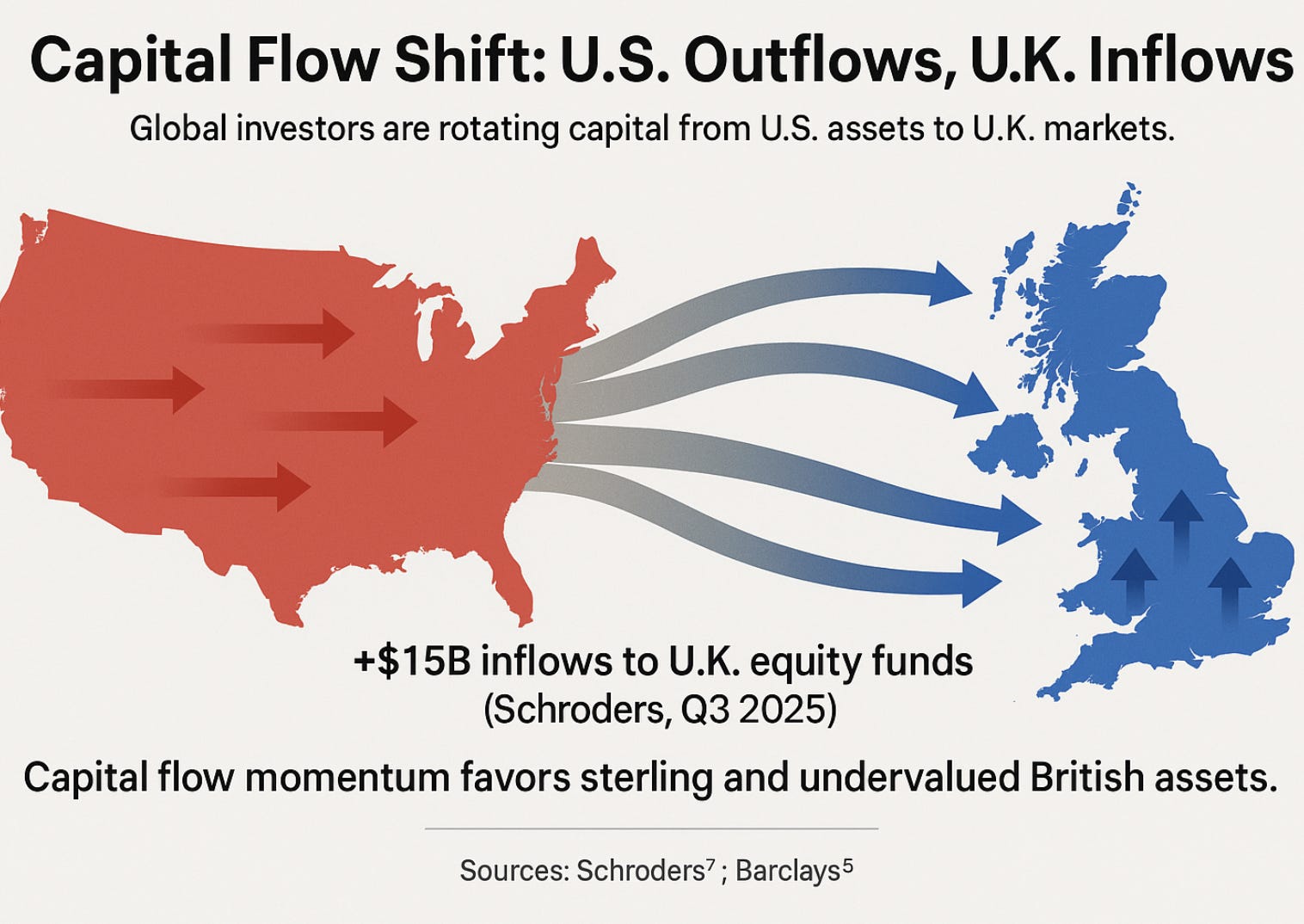

At the same time, inflows into the United Kingdom have accelerated. Analysts note that years of persistent outflows from British markets are finally easing⁶. Data from Schroders indicate roughly $15 billion of U.S. investor money has entered U.K. equity funds year-to-date⁷. After years of Brexit-related discounting, British stocks now look inexpensive relative to peers. Combined with reduced trade friction and a more predictable policy stance from the Bank of England, that value story has revived interest in London markets⁸. Some strategists argue the pound’s strength both reflects and reinforces this confidence: foreign capital dampens imported inflation and steadies domestic conditions⁹.

Not everyone shares the optimism. Certain fixed-income managers have exited U.K. government bonds, anticipating that sterling may weaken against the euro¹⁰. Their skepticism underscores the political and fiscal risks that still shadow Britain—from budget strains to leadership uncertainty. Yet even cautious investors acknowledge that the flow of funds has turned meaningfully positive.

For portfolio managers, these shifts have clear implications. A softer dollar reduces the benefit of unhedged U.S. holdings when measured in foreign currency terms, while a firmer pound enhances returns on U.K. assets¹¹. The macro takeaway is straightforward: currency allocation can be as important as stock selection. Those aligning portfolios with cross-border capital trends may find relative performance advantages—provided they remain alert to reversals. Should the Fed pause its easing cycle or Washington temper trade measures, flows could swing back toward the dollar. Conversely, renewed political turmoil in Britain could erode confidence just as quickly¹².

The recent reallocation of global liquidity thus tells a nuanced story: markets are rewarding stability and credible policy over sheer size. The dollar-short, pound-long narrative captures a broader rebalancing of capital toward undervalued regions with clearer fiscal direction. For now, the signal is unmistakable—follow the money, but keep an eye on the exit.

Footnotes

¹ Market data, Reuters, October 2025.

² U.K. Office for National Statistics; U.S. Bureau of Labor Statistics, 2025.

³ Goldman Sachs FX Strategy Note, September 2025.

⁴ Bloomberg Policy Tracker, October 2025.

⁵ J.P. Morgan Fixed Income Outlook, 2025.

⁶ Barclays Global Flows Report, 2025.

⁷ Schroders Investment Flows Update, Q3 2025.

⁸ Financial Times Markets Brief, October 2025.

⁹ Bank of England Monetary Policy Summary, September 2025.

¹⁰ Morgan Stanley FX Weekly, October 2025.

¹¹ State Street Global Advisors Currency Insights, 2025.

¹² Oxford Economics Macro Risk Monitor, October 2025.

This material presented by Dynamic Wealth Group (“DWG”) is for informational purposes only and is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy, or investment product. Facts presented have been obtained from sources believed to be reliable, however DWG cannot guarantee the accuracy or completeness of such information, and certain information presented here may have been condensed or summarized from its original source. DWG does not provide legal or tax advice, and nothing contained in these materials should be taken as legal or tax advice.