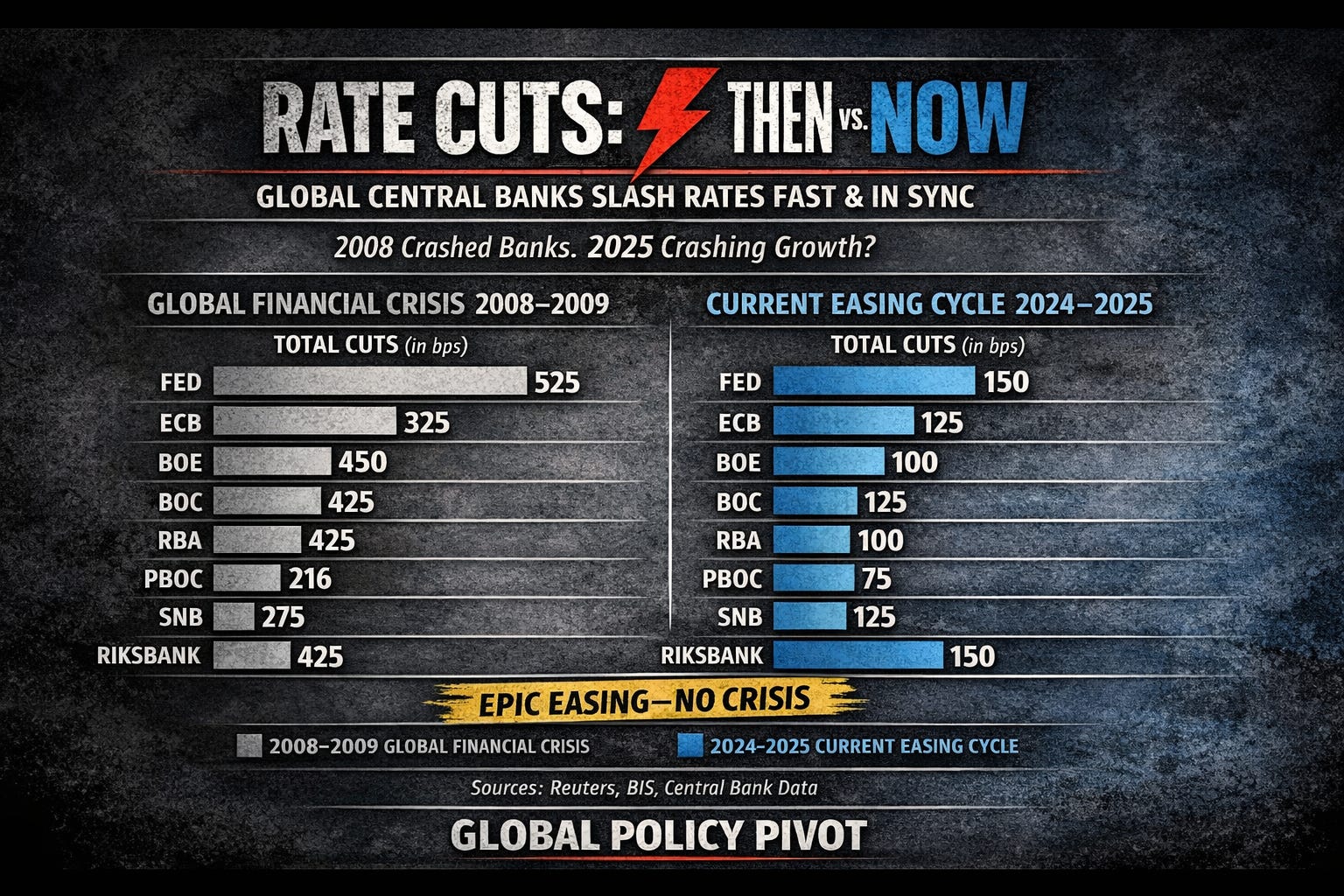

Why Global Central Banks Are Easing at a Pace Not Seen Since 2008

The global monetary backdrop shifted abruptly in 2025. After spending much of the prior two years fighting inflation with aggressive rate hikes, central banks reversed course with remarkable speed. By year-end, policymakers across the world had delivered the fastest and most synchronized round of interest-rate cuts since the aftermath of the 2008 financial crisis.¹ This pivot was not subtle. Nine of the ten central banks overseeing the most heavily traded currencies lowered policy rates in the same year, an alignment rarely seen outside periods of acute stress.¹

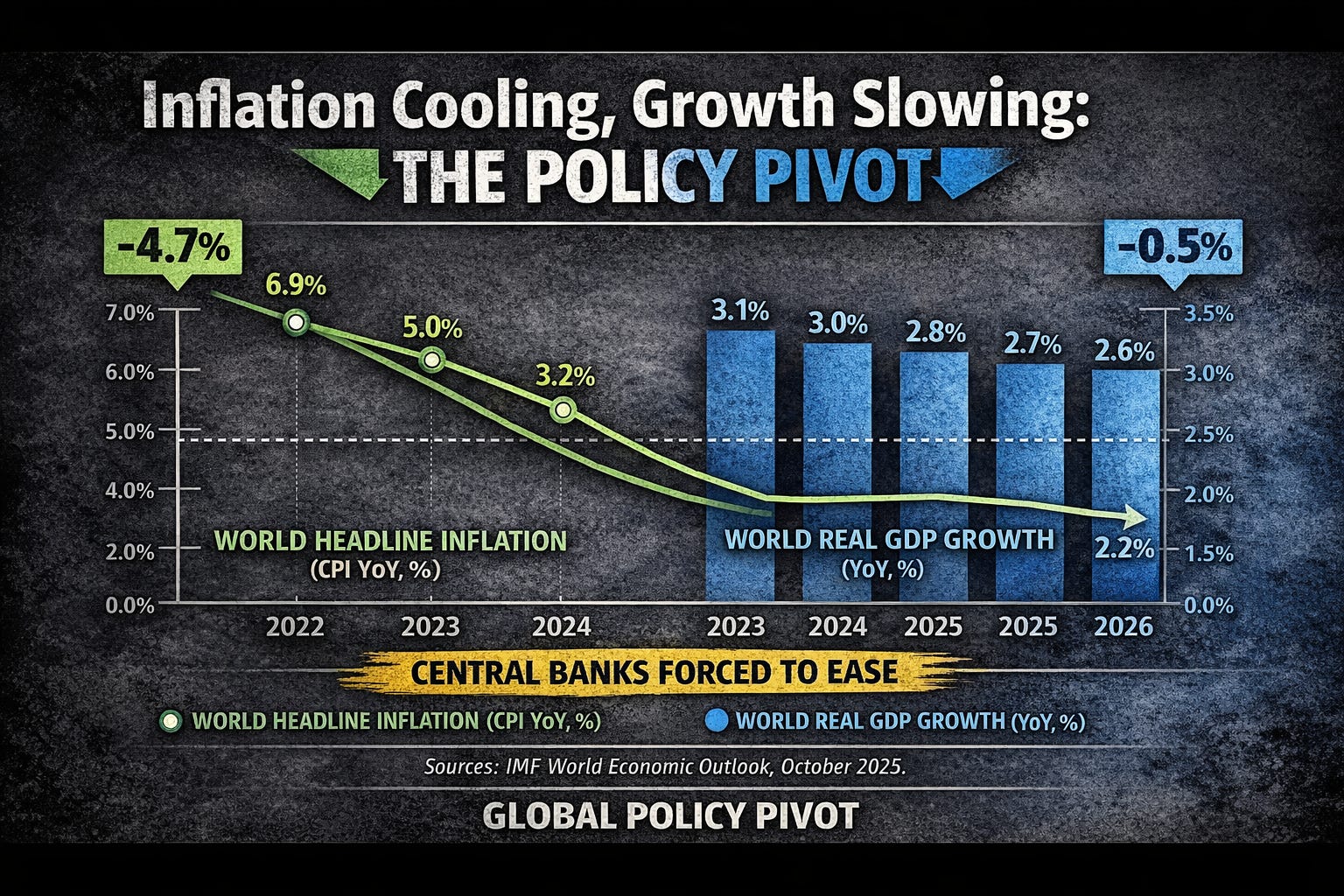

The reason for this reversal was not renewed economic strength, but rather a growing concern that restrictive policy had begun to bite too hard. Inflation pressures eased materially as energy prices stabilized and supply-side disruptions faded.²³ At the same time, signs of economic fatigue accumulated. Manufacturing activity softened, labor markets cooled, and business sentiment weakened across multiple regions.⁴ By late 2024, central banks increasingly judged that the risk of overtightening outweighed the risk of allowing inflation to linger modestly above target.²

From Inflation Control to Growth Preservation

This shift marked a clear transition from inflation control to growth preservation. Rather than waiting for recessionary conditions to fully materialize, policymakers moved pre-emptively. Rate cuts were framed as insurance against a sharper downturn rather than stimulus aimed at overheating demand. Central bank communications increasingly emphasized downside risks to growth, tighter financial conditions, and the lagged effects of earlier tightening.³⁴ Japan stood out as a rare exception, tightening policy modestly amid domestic wage pressures, but the broader global trend was unmistakable.¹ Central banks concluded that maintaining restrictive settings for too long risked turning a slowdown into something more severe.⁴

Markets responded quickly. Bond yields declined across developed and emerging economies, driving a broad rally in fixed income. Emerging-market debt benefited in particular as lower global rates reopened capital flows that had been constrained during the tightening cycle. Sovereign spreads compressed meaningfully as investors reached for yield in a more accommodative environment.⁵⁶ In developed markets, government bonds also caught a bid as expectations for prolonged policy restraint faded.⁶

Cross-Asset Implications and Investor Considerations

Equities were even more sensitive to the shift. Global stock markets advanced largely on the back of easier financial conditions rather than improving fundamentals. Liquidity, rather than earnings growth, became the dominant driver of returns.⁷⁸ Sectors most sensitive to interest rates, including technology and housing-related equities, saw renewed investor interest as discount rates declined. The familiar refrain of “don’t fight the central bank” reasserted itself.⁸

Currency markets told a more nuanced story. The euro and British pound weakened as policy in Europe turned more accommodative, while the U.S. dollar proved more resilient than many expected. Even after rate cuts, U.S. yields remained relatively attractive, and the dollar’s role as a perceived safe haven helped offset dovish policy signals.⁸⁹

For investors, the implications are mixed. Easier policy has clearly supported asset prices, but it also reflects a more fragile economic backdrop. Liquidity can lift markets in the short run, yet it cannot guarantee durable growth. History suggests that rallies driven primarily by monetary easing, rather than improving fundamentals, can be vulnerable if confidence falters.⁷¹⁰ The current environment rewards flexibility and discipline. Central banks have stepped forcefully back into the spotlight, but their actions underscore caution rather than celebration.

Footnotes

Karin Strohecker and Sumanta Sen, “Major Central Banks Deliver Biggest Easing Push in Over a Decade in 2025,” Reuters, December 23, 2025.

European Central Bank, “Monetary Policy Decisions,” press release, December 14, 2025.

U.S. Federal Reserve, “Federal Open Market Committee Statement,” press release, December 13, 2025.

Bank for International Settlements, Annual Economic Report 2025 (Basel: Bank for International Settlements, June 30, 2025).

State Street Investment Management, “Emerging Market Debt Market Commentary: October 2025,” November 26, 2025.

International Monetary Fund, Global Financial Stability Report: Navigating Monetary Turning Points (Washington, DC: International Monetary Fund, October 10, 2025).

Hou Zhenhai, “Global Dual Fiscal and Monetary Easing Is Expected to Continue in 2026,” Straits Financial Group, December 16, 2025.

Morgan Stanley Research, “2026 Investment Outlook: U.S. Stocks Shine in Spotlight of Favorable Conditions,” November 19, 2025.

Organisation for Economic Co-operation and Development, OECD Economic Outlook, Volume 2025 Issue 2 (Paris: OECD Publishing, November 28, 2025).

World Bank, Global Economic Prospects (Washington, DC: World Bank, January 9, 2025).

This material presented by Dynamic Wealth Group (“DWG”) is for informational purposes only and is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy, or investment product. Facts presented have been obtained from sources believed to be reliable, however DWG cannot guarantee the accuracy or completeness of such information, and certain information presented here may have been condensed or summarized from its original source. DWG does not provide legal or tax advice, and nothing contained in these materials should be taken as legal or tax advice.